Global Monetary Base - Update through November 2024 and 2025 Forecast

- InfraCap Management

- Dec 4, 2024

- 2 min read

Updated: Feb 1

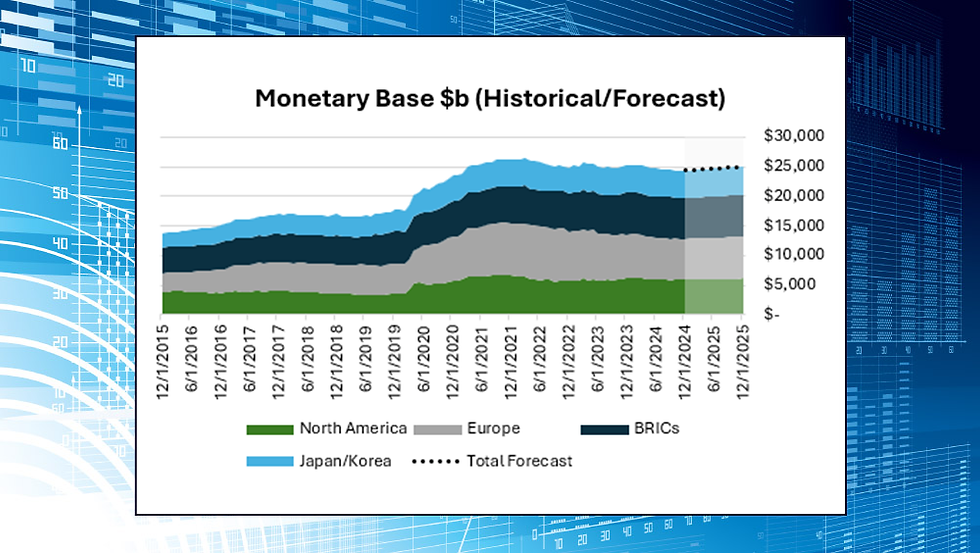

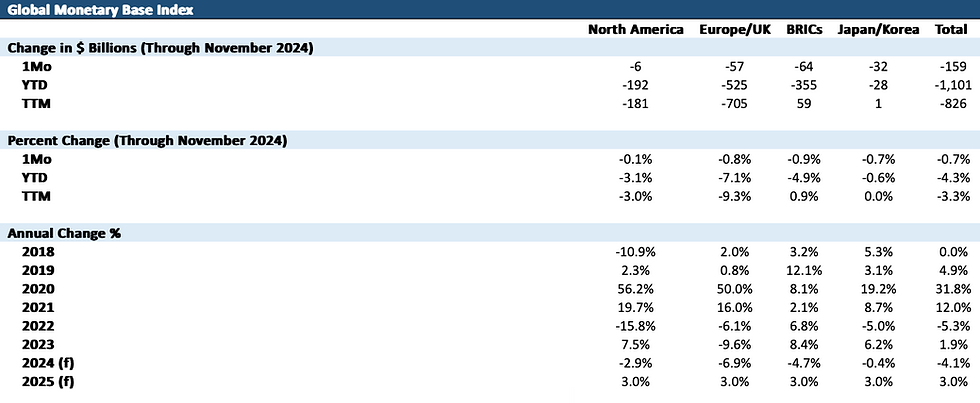

InfraCap Report Update, New York, NY ~ The team at Infrastructure Capital Advisors tracks the Global Monetary Base, defined as currency in circulation plus bank reserves, as an indicator of current and future interest rates. This article provides data and insights for November 2024 data released in December.

November Global Monetary Base (GMB):

GMB was down 0.7% in November and was lower by $830 billion over the last twelve months. We believe that tight global monetary policy was the key driver of higher global rates and not the increase in US treasury issuance. Our view is supported by the fact that U.S. rates dropped by 12 basis points in November, as it became apparent that the Fed’s tightening cycle was over.

We expect that the GMB will stabilize over the next quarter and start growing in 2025 as the European Central Bank (ECB) and the Peoples Bank of China (PBOC) are forced to ease monetary policy in response to a recession in Europe and slow growth in China. Eurozone GDP increased 0.4 % in the third quarter of 2024, in line with expectations. Low European growth is not surprising considering the ultra-tight ECB policy and the absence of the positive dynamics that are supporting the US economy, including an 80% cost advantage in natural and gas and electricity costs and counter-cyclical infrastructure spending.

If the Global Monetary Base remains flat through the beginning of 2025, we expect interest rates to also stabilize and decline in the first half of 2025 as central banks cut rates in response to slow or negative growth. Declining global interest rates and a flat to increasing GMB will support the global stock and bond markets.

Comments