September 2025 Commentary and Economic Outlook

- InfraCap Management

- Sep 16, 2025

- 4 min read

SEPTEMBER 2025 EDITION:

Commentary and Economic Outlook

Scroll to read full report or click below to skip to specific sections:

MARKET & ECONOMIC OUTLOOK WEBINARBe sure to register and attend our Monthly Market & Economic Outlook Webinar scheduled for Thursday, September 18th 2025 @ 1:30PM EDT. In the webinar, Jay Hatfield, Infrastructure Capital Advisors CEO and Portfolio Manager, will walk you through updated market commentary, and economic outlook for the coming months. SIGN UP! |

| Economy: |

The monetary base is the critical leading indicator of inflation and GDP growth. M1 and M2 have become outdated indicators after the GFC as banks now have massive excess reserves so the Fed can no longer control the size of bank balance sheets to restrict credit. In addition, non-bank lending has growth exponentially, further limiting the importance of M1 and M2 relatively to the monetary base.

The monetary base is flat Y/Y vs. a normal growth rate of 5% which is deflationary and could lead to a recession.

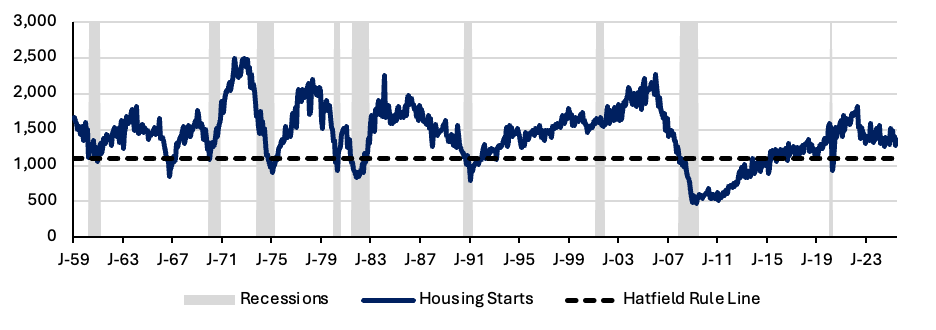

The only reason the US economy is not in recession is the housing sector has become less cyclical as home building has remained muted since the GFC with only an average of 1.1MM homes started with a peak of 1.8MM. During the 10 years prior to the GFC, starts averaged 1.7MM with a peak of 2.3MM.

The “Hatfield Rule” is a recession indicator which states that if housing starts drop below 1.1MM there will be a recession. It is superior to the “Sahm” rule as housing is a leading indicator and employment is a lagging indicator.

Consequently, there is a significant shortage of homes in the US of approximately 4MM homes. Also, there is now an active group of investors buying new homes to rent which provides for more resilient demand than has existed in the past. A decline in the housing sector accounted for 12 out of 13 post WWII recessions.

We publish a real time CPI estimate that calculates the shelter component of CPI utilizing real time, national data from Zillow and Apartment list.

CPI-R continues to be a be below CPI-U (Core CPI) and has been a reliable predictor of CPI-U.

In addition, employment growth has stalled with less than 35k jobs created on average over the last 3 months according to the employer survey and over 850k jobs lost according to the household survey. Continuing claims also remain elevated at almost 2MM.

Private investment GDP drives economic cycles.

Tariffs are positive for economic growth in the medium to long term as the additional revenue from tariffs reduces the federal budget deficit and crowding out of private investment. Savings and investment are 70% correlated with GDP growth globally according to an IMF study.

We forecast that the Federal Budget deficit declines to $1.3 Trillion in Fiscal 26 with tariffs contributing $350 billion of incremental revenue based on an expected average tariff rate of 20%.

| Stock Market: |

We are raising our S&P 500 Index year end 2025 target from 6,600 to 7,000 based on both continuing momentum in AI related earnings growth and increased visibility on Fed Rate cuts. Our target assumes a 23x multiple of 2026 S&P earnings of 305.

We are also initiating a 2026 year-end target for the S&P of 7,700 based on a 23x multiple of our 2027 S&P earnings per share estimate of $335.

Given the decline in rates and our bullish outlook on stocks, we recommend large cap dividend stocks, small cap stocks and high yield fixed income.

| Bond Market: |

We project that the 10-year treasury trades in the 3.5 - 4.0% range as the terminal rate of expected Fed funds trends down to the 2.75% area as reported inflation slowly reflects the decline in real time inflation.

The economy is slowing and weakness in the US job market will likely force the Fed to cut 2-3 times this year. GDP growth has only averaged 1.5% this year and the interest sensitive construction and residential sectors have contracted over the last year in response to tight Fed policy.

Importantly, 2 members of the 7-member Federal Reserve Board came out for a July rate cut. The market had failed to recognize that tariffs are recessionary/deflationary as the tax revenue reduces the deficit.

US 10-year bonds are 70% correlated to the expected terminal Fed Funds rate and 25% correlated to global bonds (see attached slide). The budget deficit is relatively static and has been in the 5% of GDP range for years, so not a driver of interest rates in the short to medium term.

Market implied policy rate continues to forecast 10-year yields with a 1% average spread.

We recommend investors add high yield bonds and preferred stocks as we do not expect a big increase in defaults and we expect treasury rates to decline below 4% as the economy weakens.

| Commodities |

We lowered our 2025 target on oil from $80 to $70 (range of $60-80) as it has become clear that Trump will use his influence with the Saudis and Russia to limit price increases despite tighter sanction on Iran. This policy will offset a good portion of one-time price increases from tariffs. We do not expect an increase in US production. We do see support for oil below $60 as most forecasters ignore the price elasticity of supply and demand for oil. Middle East wars will only impact prices if oil production facilities are destroyed.

Artificial Intelligence and data centers have opened new growth prospects for natural gas midstream companies to supply gas fired power plants. Natural gas plants have some of the shortest times to build and we believe they are best positioned to supply reliable power quickly.

Comments